For modern organizations, it is essential to have methods for collecting data and making decisions based on the strategic objectives that lead to the achievement of competitive advantage. The balanced scorecard (BSC) represents strategic planning and management that companies use for communicating their intended accomplishments, aligning everyday procedures with the formulates strategy, monitoring progress, and prioritizing projects. In general, BSC is used for measuring and providing feedback to organizations, with data collection being crucial to the provision of quantitative results. This data is interpreted by managers and executives who make further decisions for an organization.

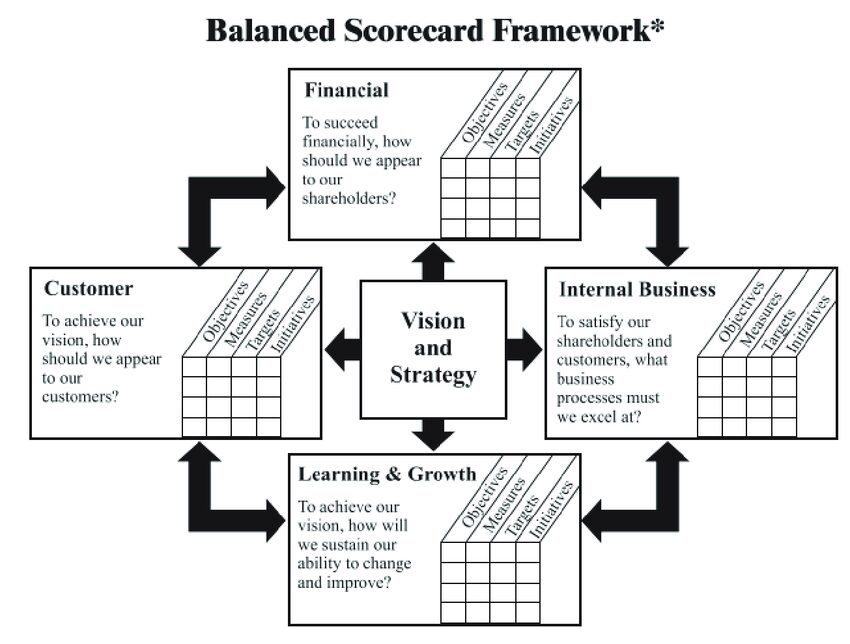

The concept of Balanced Scorecard (BSC) was first introduced by Kaplan and Norton who received great praise for their research. The key principle behind the concept lies in finding balance across all functions of an organization since the majority of companies focus on financial measures such as growth and profitability, forgetting about such sectors as internal processes, customers, and organizational capacity. By looking at business across four perspectives, organizations can understand causal relationships between investment and the financial outcome can be identified, measured, and managed. Therefore, BSC is not a regular scorecard but a methodology that enables organizations to look at both financial and non-financial objectives that are associated with strategic priorities. This means that organizations are forced to think about how they can measure their objectives and identify projects that will help drive those objectives.

To understand Balanced Scorecard (BSC) further and proceed with its critique, it is essential to understand the four perspectives involved in it. The financial perspective is linked to the range of monetary objectives and measures that organizations use for answering the question of how a business looks to its shareholders. Usually, these objectives are the easiest to define and measure. Although, creating a financial objective, such as Improve Profit, is not enough for helping organizations understand how they can achieve these goals. The customer perspective is concerned with measures that are directly related to companies’ clients with a specific focus placed on their satisfaction. Organizations should answer the question of how their clients see them understand what they want and what can be done to fulfill their desires.

The perspective of internal processes is associated with objectives and measures which determine how well an organization is running as well as whether the offered products and services align with what customers require. This means that some of the costs can be reduced by streamlining some of the internal processes. Lastly, the organizational capacity perspective is associated with measures and objectives that show how workers within a company perform and how their skills align with the existing infrastructure and technology. Nevertheless, despite the range of benefits provided by BSC, the focus of the current discussion will be placed on determining the limitations of the principle.

General Issues with BSC Implementation at Organizations

In day-to-day use, some problems prevent organizations from accessing necessary data and make decisions based on them. The key issue with balanced scorecards is that they do not offer practical guidance for deployment and too many users view it as a ‘quick fix that can be easily integrated into the processes within organizations. Besides, many managers fail to understand that the implementation of a balanced metrics system is an evolutionary process and not a one-step task that can be quickly marked as ‘completed.’ If managers do not recognize this issue related to BSC implementation, they are more likely to fail to dedicate efforts to long-term positive results for their organizations. As a result of the implementation of BSC at organizations, it became possible to identify issues in their use and reasons that contribute to the failure of balanced scorecard initiatives.

Inadequately-Defined Metrics

In organizational contexts, metrics refer to measures used for assessing the performance of workers, activities involved in the accomplishment of corporate goals, and general behaviors that exist within companies. Metrics are used for measuring how well an organization is doing and whether it accomplishes the established objectives. This means that measures should be relevant to the environment in which they are applied. To ensure that workers understand the expectations of their achievements, metrics should be depicted as visual indicators as well as should be collected at a perfect frequency for decision-making. In addition, measures should be defined in such a way that they can be consistently used across all departments of a company, even in cases when their performance targets differ from one another. A system that has inconsistencies in the definition of metrics is highly likely to be vulnerable to criticism from employees who want to avoid accountability.

The Absence of Efficient Collection and Reporting

One of the main reasons behind companies over-emphasizing their financial metrics at the cost of other important variables refers to the already existing systems of collecting and reporting financial measures. Organizations that intentionally plan to define several crucial metrics and dedicate resources for automating data collection and its subsequent reporting usually achieve positive results. However, in the majority of companies, if the process of data collection takes too much time, even the most vital metrics will not be captured. This explains the need for prioritizing key performance indicators (KPIs) in an organizational context to ensure that organizations investment in metrics is concerned with gathering relevant information that will be vital to improving performance. Therefore, BSC requires executives to invest in efficient data collection and measurement procedures for the successful integration of the model in the everyday tasks of organizations.

Excessive Focus on Internal Processes

Balanced scorecard methodology has received extensive criticism due to its specific focus on internal processes within companies. Although, this issue is associated not with the method itself but rather with the way that it is being put into practice. For companies to avoid this limitation of BSC, it is recommended that managers start with an external focus to view organizations as a system. In this case, the goal is achieving a balance of enterprise-level metrics as organizations assess their market, competitors, shareholders, employees, and stakeholders.

It is also recommended to collect and assess data in regards to a company’s strengths, weaknesses, opportunities, and threats (SWOT). A SWOT analysis should be incorporated in the measurement of the well-being of a company because it accounts for both internal and external components that contribute to the competitiveness of an organization. As applied to BSC, SWOT indicators will guide organizations to identify enterprise-level metrics that will be used for later analysis. By combining both internal and external factors that affect companies, it is possible to test the alignment of metrics that influence the shaping of performance drivers. However, when companies use BSC without paying attention to external factors that influence their success, they risk suffering from the limitations of balanced scorecards that make them focus on internal processes, which are not enough for achieving competitiveness.

The Absence of a Formal Review Structure

Formal organizational reviews represent ways to guide in regards to the organization structure, organization culture, as well as building and managing work in teams. Assessing the organizational structure of companies is essential for businesses of any type and size because they offer clarity and guidance on specific human resource issues, including managerial authority. Small-scale businesses are also recommended to consider their formal structure to ensure the sustainability of processes at the growth stages of their business. In regards to the use of scorecards, their effectiveness relies on frequent reviews to make a difference. If the value of metrics changes regularly and the variables within the management’s control can be affected daily, such measures should also be frequently reviewed. Besides, meetings that focus on metrics review should follow a standardized agenda, with clearly defined roles for everyone involved in them. This can result in positive outcomes as all relevant metrics are monitored while all actions are agreed upon within the collaborative environment.

It is also worthy of mentioning that reviews of metrics should be cross-functional and include peer groups that have a shared responsibility for process results. For BSC systems to work effectively, those involved in process reviews should participate in the creation of a new system of measurements. This calls for significant behavioral change as early as possible to aid companies to define, automate, and deploy metrics measurement. Overall, to overcome the challenges of BSC implementation, organizations should establish formal review structures first and integrate the system based on the findings of these reviews.

Issues with Achieving Positive Outcomes

Companies have been challenged by the issue of balanced scorecards not resulting in positive outcomes. This problem is associated with the fact that many managers treat the framework as if it is a technical solution for providing measures. Therefore, not much attention is given to the social aspect of information collection and assessment as well as how this information can influence the decision-making process. Many BSC initiatives are implemented without significant progress being made, which means that they do not change what they were intended to change. In some cases, BSC integration results in negative outcomes such as decreased productivity of workers who were resistant to change.

Limitations in the achievement of BSC success are often associated with the latter not contributing to informed decisions. Thus, if the management of organizations has scorecards that are collected and reported on but that are never used for making relevant decisions about the businesses, then BSC has been implemented incorrectly. The key purpose of BSC integration into business processes is associated with making good decisions and then executing them correctly. It is suggested for managers to look at the model that they have integrated into the workplace setting and identify points that will make the processes better. Looking at the bottom line when implementing balanced scorecards is imperative: companies spend a lot of money on their integration, which means that all processes involved in it should go smoothly without any time and effort being wasted.