Once the target firm has been identified and valued, the acquisition moves forward into the structuring phase. There are three interrelated steps in this phase. The first is the decision on how much to pay for the target firm, synergy and control built into the valuation. The second is the determination of how to pay for the deal, i.e., whether to use stock, cash or some combination of the two, and whether to borrow any of the funds needed. The final step is the choice of the accounting treatment of the deal because it can affect both taxes paid by stockholders in the target firm and how the purchase is accounted for in the acquiring firm’s income statement and balance sheets. Deciding on an Acquisition Price The value determined in consideration of synergy and control represents a ceiling on the price that the acquirer can pay on the acquisition rather Continue reading

Corporate Strategies

Case Study: How IBM Championing Social Media Adoption in Business?

International Business Machines Corporation, or the IBM, is basically a multinational computer technology and has got hold over IT consulting services. The company has established itself as one of the selected information technology companies since 19th century. With its growth in the manufacturing as well as marketing domains of computer hardware and software, it has gained the nickname of “Big Blue”. IBM had encouraged its employees to use internet since 1997 when most of the companies were not allowing their employees use of internet. In 2003, the company made a strategic decision to encourage IBMers to participate in blogs and embrace the blogosphere. Social Business @ IBM is an internal site that has interactive, educational and social programs which explain IBM’s social business transformation and educates and enables IBMers in external social media participation. Employees take personal responsibility for their social media activities and the company has set Continue reading

Divestitures in Business – Concept, Reasons, and Benefits

In the modern world, so many organizations are using several strategies to enhance their performance and improve their competitive advantages. Some of the mostly relied on strategies are divestitures or mergers & acquisitions. The two though somehow different have some similarities. Mergers and Acquisitions refers to two companies combining together to form a single entity or one parent company absorbing another company and completely eliminating the entity of the target company to incorporate its operations in the parent company. Divestitures or rather divestment on the other hand is the opposite of investment and refers to the reduction/addition of the firm’s partial assets or complete sale of an existing business by a firm due to some ethical or business reasons. One of the reasons behind the above corporate strategies is to increase the firm’s chances of survival in a market environment characterized by many competitors and in particular perfect market industry. This is Continue reading

Foreign Market Entry Modes – Five Modes of Foreign Market Entry

Changes in the internal and external business environment have meant that more and more firms are expanding their operations across country borders. External factors such as: the removal of trade barriers, free trade agreements between countries, and an emerging middle class has made the idea of going global more attractive to organisations across the world. Internal factors such as: increasing profits, increasing market share and becoming a global brand are more drivers for organisations to globalize. Whilst there are a lot of drivers of internationalization, and hence potential advantages to internationalize. Types of Foreign Market Entry Modes An organisation has a number of different entry modes to choose from when it internationalizes its operations. All organisations will have different reasons for going global, which will have an influence on which entry mode is best suited to them. An organisation will need to determine their desired level of commitment, flexibility, control, Continue reading

Resource Based View (RBV) and Sustainable Competitive Advantage

Resource based view (RBV) focuses on the internal factors that contribute to a firm’s growth and performance. It highlights the importance of firm’s resources and capabilities. Both of them will together form a competency that can create a competitive advantage. Resources can also be divided into tangible resources and intangible resources. Capabilities of the firm in utilizing the resources have a big impact on how a firm will be able to stand out among other competitors. Competitive advantage arises when a firm has a lower cost structure, products differentiation and niche markets. RBV also concerns in value creation in order to compete with others. On the other hand, in order to survive in this competitive world, a firm needs to fully prepare itself to achieve sustainable competitive advantage (SCA), which means having a superior performance in a longer term compared to other rivals. According to Jay Barney (1991), resources need Continue reading

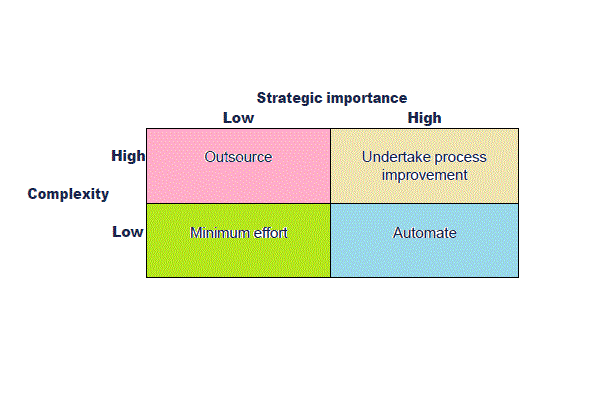

Harmon’s Process-Strategy Matrix

Process-Strategy matrix by Paul Harmon will be useful in deciding how the process should be managed, it gives two variable one Is importance and other is complexity and dynamics. There may be other variables to consider in practice such as culture, cost and savings and quality. It should be used flexibly by considering all the variable affecting the current and future prospects of the organization. Advantages and disadvantages should be considered before reaching the final decision. How To Assess The strategic Importance? Strategic importance can be assessed by asking what would happen if a process is abandoned. If it impacts the business objective (Quality, cost control and reputation etc.) materially (more than insignificant) than it can be assessed as high strategic importance like threatening to the survival of business. Strategic importance can also be assessed by identifying key stakeholders. If the process affecting the key stakeholders like customers, Tax authorities Continue reading