System of Planned Economy Under the conditions of the planned economy, all decisions concerning what to manufacture, how to manufacture and to whom to manufacture are approved by the sole center or group. This economy is based on collective ownership. Fixed production assets are owned by the government, and resources, production and the quantities of future products are distributed according to a plan. The type of the system of the command economy was prevailing in the USSR, Cuba, and North Korea. The plans of the system of the centralized economy are drawn up and implemented by the authorities and governmental political leaders after consulting with highly ranked professionals: engineers, economists, industrialists, and other experts. These planners decide which products to manufacture and which services to render. Their vote is decisive in approving decisions whether new undertakings are to be constructed, how many employees are to be employed at undertakings, whether Continue reading

Economics Basics

Laws of Returns in Economics

The relationship between the inputs and the output in the process of production is clearly explained by the Laws of Returns or the Law of Variable Proportions. This law examines the production function with only one factor variable, keeping the quantities of other factors constant. The laws of returns comprise of three phases: The Law of Increasing Returns. The Law of Constant Returns. The Law of Diminishing Returns. The Laws of Returns in Economics may be stated as follows: “If in any process of production, the factors of production are so combined that if the varying quantity of one factor is combined with the fixed quantity of other factor (or factors), then there will be three tendencies about the additional output or marginal returns: Firstly, in the beginning, as more and more units of a variable factor are added to the units of a fixed factor, the additional Continue reading

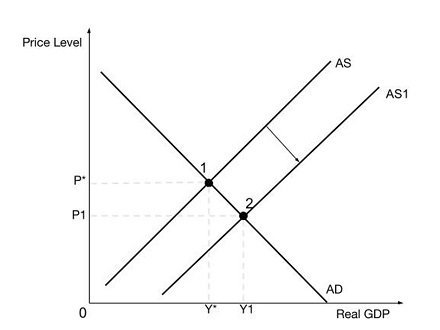

Role of Supply Side Policies in Balanced Economic Growth

The government has a responsibility for delivering public goods optimally for the collective development of all individuals. In the quest to achieve this noble course, supply side policies, which form part of macroeconomic strategies, are developed to ensure that markets and industries function in an efficient way to increase the rate of economic growth as reflected in the real national yield. Many governments support the assertion that they can achieve a sustained economic growth by improving supply side operations without causing an increase in inflation. However, reforms on the supply side policies do not facilitate the achievement of adequate growth. Definition and Explanation of Balanced Economic Growth Although the growth rate does not reflect people’s living standards entirely, economic growth has been one of the critical areas of consideration for every nation that is in the process of developing its economic policies. Indeed, economic growth is the most common approach Continue reading

Concept of Demand in Managerial Economics

In Economics, use of the word ‘demand’ is made to show the relationship between the prices of a commodity and the amounts of the commodity which consumers want to purchase at those price. Definition of Demand: Hibdon defines, “Demand means the various quantities of goods that would be purchased per time period at different prices in a given market.” Bober defines, “By demand we mean the various quantities of given commodity or service which consumers would buy in one market in a given period of time at various prices, or at various incomes, or at various prices of related goods.” Demand for product implies: a) desires to acquire it, b) willingness to pay for it, and c) Ability to pay for it. All three must be checked to identify and establish demand. For example : A poor man’s desires to stay in a five-star hotel room and his willingness to Continue reading

Economic Tools for Management Decision Making

Managerial decision-making draws on economic concepts as well as tools and techniques of analysis provided by decision sciences. The major categories of these tools and techniques are optimization, statistical estimation and forecasting. Most of these methodologies are technical. These methods are briefly explained below to illustrate how tools of decision sciences are used in managerial decision making. 1. Optimization Optimization techniques are probably the most crucial to managerial decision making. Given that alternative courses of action are available, the manager attempts to produce the most optimal decision, consistent with stated managerial objectives. Thus, an optimization problem can be stated as maximizing an objective (called the objective function by mathematicians) subject to specified constraints. In determining the output level consistent with the maximum profit, the firm maximizes profits, constrained by cost and capacity considerations. While a manager does not resolve the optimization problem, he or she may make use of the Continue reading

Basic Economic Tools in Managerial Economics for Decision Making

Business decision making is essentially a process of selecting the best out of alternative opportunities open to the firm. The steps below put managers analytical ability to test and determine the appropriateness and validity of decisions in the modern business world. Following are the various steps in decision making process: Establish objectives Specify the decision problem Identify the alternatives Evaluate alternatives Select the best alternatives Implement the decision Monitor the performance Modern business conditions are changing so fast and becoming so competitive and complex that personal business sense, intuition and experience alone are not sufficient to make appropriate business decisions. It is in this area of decision making that economic theories and tools of economic analysis contribute a great deal. Basic Economic Tools in Managerial Economics for Decision Making Economic theory offers a variety of concepts and analytical tools which can be of considerable assistance to the managers in his Continue reading