Poverty – A Multidimensional Phenomenon Poverty has many faces, and multiple indicators are used to capture the different deprivations experienced by a population. This complex phenomenon is linked to economic wellbeing, capability, and social exclusion. Poverty is a major moral problem because of the suffering it causes and the disadvantages conferred to some population segments. It is defined as a persistent and debilitating social condition attributed to diverse causes that affect a person’s physical, mental, and emotional wellbeing. The complex nature of poverty means that multiple measures are used depending on a country’s priorities. 1. Economic Wellbeing Income and consumption are key quantifiable indicators of poverty in society. These variables measure economic wellbeing and contain absolute, relative, and subjective components. At the basic level is absolute poverty, which describes the lack of necessities needed for survival – shelter, clean water, and food. Here, the quality of survival is an important Continue reading

Economics Concepts

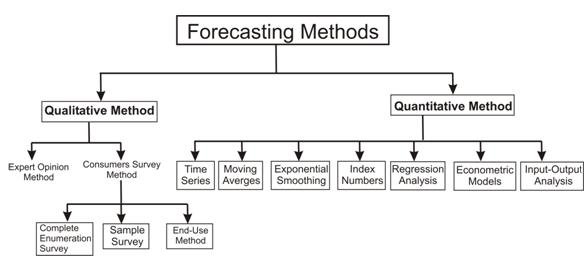

Expert Opinion Method of Demand Forecasting

In this method of demand forecasting, the firm makes an effort to obtain the opinion of experts who have long standing experience in the field of enquiry related to the product under consideration. If the forecast is based on the opinion of several experts then the approach is called forecasting through the use of panel consensus. Although the panel consensus method usually results in forecasts that embody the collective wisdom of consulted experts, it may be at times unfavorably affected by the force of personality of one or few key individuals. To counter this disadvantage of panel consensus, another approach is developed called the Delphi method. In this method a panel of experts is individually presented a series of questions pertaining to the forecasting problem. Responses acquired from the experts are analyzed by an independent party that will provide the feedback to the panel members. Based on the responses of Continue reading

Supply Side Policies – Meaning, Definition, and Categories

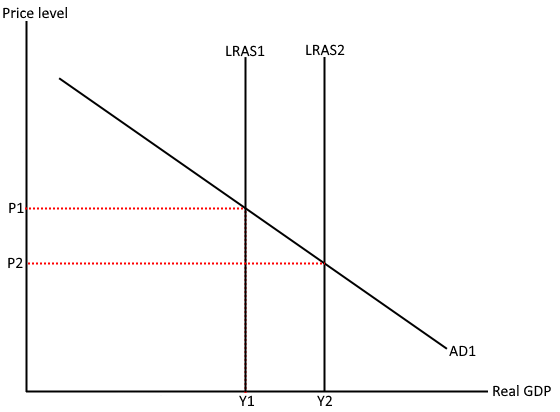

The supply side policies entail the attempts undertaken by governments in an effort to stimulate productivity and ensure that the long-term aggregate supply [LRAS] curve shifts to the right as illustrated in graph 1 below. The outward shift of the LRAS curve leads to an increase in the potential output. From the graph, the shift in the LRAS to LRAS2 leads to an increase in the size of the output from Y1 to Y2. The supply side policies are focused on stimulating a country’s productive capacity. Labor productivity is one of the most important elements in the supply side policies. The policies underscore the importance of establishing flexible labor markets. Despite the flexibility aspect, the role of the government in the implementation of the supply side policies cannot be ruled out. In some instances, government intervention is necessary in order to overcome market failure. The objective of the supply side Continue reading

Profit Maximization Model in Managerial Economics

Profit-making is one of the most traditional, basic and major objectives of a firm. Profit-making is the driving-force behind all business activities of a company. It is the primary measure of success or failure of a firm in the market. Profit earning capacity indicates the position, performance and status of a firm in the market. It is an acid test of economic ability and performance of an individual firm. There is no place for a firm unless it earns a reasonable amount of profit in the business. It is necessary to stay in business and maintain in tact the wealth producing agents. It is a widely accepted goal and there is nothing bad or immoral about it. Earlier profit maximization was the sole objective of a firm. This assumption has a long history in economic literature and the conventional price theory was based on this very assumption about profit making. Continue reading

Different Approaches to Profit in Managerial Economics

Profit is the reward which goes to organization as a factor of production for its participation in the process of production. Profits differ from other factor rewards in the following ways: Profit is a residual income left after the payment of contractual rewards to other factors of production. The entrepreneur while hiring other factors of production enters into contract with them. He pays wages to workers, rent for land and interest for borrowed capital and the residue or whatever is left is his profit. Thus profits become non-contractual in character. The various factors of production are rewarded even before the sale of the product and irrespective of its sales whereas profits accrue only after the product is sold. The rewards of other factors have been fixed. They do not fluctuate whereas profits go on fluctuating so much so that the entrepreneur bears the risk of even incurring losses which we Continue reading

Impact of Banking Regulations on Financial Intermediation

Banks have all along played the role of financial intermediaries by channelizing funds primarily from the household sector to producing sector and the efficiency and smoothness with which such intermediation is done by banks are one of the prime parameters that determine the economic efficiency and consequent industrial and material progress of a society. Financial intermediation has a cost and that cost is reflected in bank rates and overhead expenditures incurred by banks. Bank rates, however, are not determined in isolation or only from the perspective of profit maximization by the banking sector. These rates are impacted by many other economic and statutory issues pertaining to a particular economy and such issues may vary widely from economy to economy depending upon the administrative attitude towards matters of equanimity in various sectors of the economy, especially the banking sector itself. The general view among experts in this field is that if Continue reading