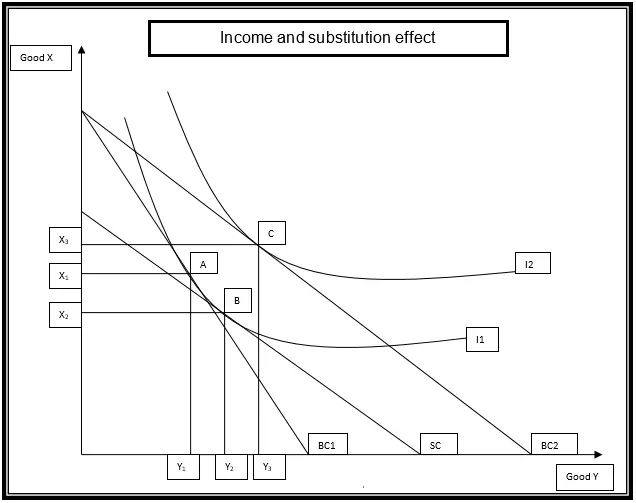

Based on the law of demand, a change in price can be described in terms of income and substitution effect. The diagram presented below will be used to explain these effects. The two items that will be analyzed are commodity Y and X. According to the law of demand, a drop in the price of commodity Y will lead to an increase in quantity demand. The increase will cause the budget line to pivot from BC1 to BC2. Also, the indifference curve will shift from I1 to I2. This represents a movement to a higher indifference curve. The equilibrium position is the point of tangency between the budget line and the indifference curve. When the price of commodity Y falls, a consumer will be indifferent between consumption at point A and B because they lie on the same indifference curve. However, at point B, the consumer shall not have exploited Continue reading

Economics Principles

Diverse Production Modes Beyond Capitalism in Global Economy

Despite the predominance of capitalism as the mode of production in the current global economy, communism, independent production, slavery and feudalism have remained active in the production modes in the society. This analytical treatise attempts to explicitly explore the tenet of existence of other modes of production besides capitalism in the present society. Through the universal principles of intelligible strategies, governments across the globe are keen on production interventions that aim at protecting the infant companies. The governments operating on this assumption have to ensure their own survival by protecting their industries and trade policies. This action represents the communist production mode which is characterized by the need to serve self interest above the interest of the competitors. The prime principle of communism is featured by interconnected holistic phenomenon. The conscientious citizenship needs to perceive the global interrelationship since the world is marked with inclusive model of integration; the world explores several Continue reading

Trickle-Down Economics or Reaganomics

In economics and politics, the term trickle-down economics or Reaganomics is the pejorative term for the theory that taxing the wealthiest individuals in society less will in allow those individuals to invest more of their money into the economics development and create new jobs for the middle and lower class. Proponents for the theory use the term supply-side economy, considering that the idea of the middle to lower classes tangentially receiving benefits through economics policy which directly benefit the rich is somewhat insulting. The basic idea is that the recipients of the tax cuts will then be able to invest more money into infrastructure, opening more stores and companies, which will then provide more jobs as well as drive down the prices of goods. However, in terms of economic theory, there have been no major economists who have ever supported this theory or have attempted to defend the “trickle-down” aspect Continue reading

Effect of Price Controls on an Economy

A lot has been said about open economies but the fact is that their existence is only in theory. It is common knowledge that all countries in the world have some entry restrictions in their markets. With this in mind, open economies are described as those countries whose policies allow production and pricing to be determined by the forces of supply and demand. The aforementioned restrictions are, therefore, in the form of policies that countries develop in a bid to accelerate economic growth. One of such policies is price control in which a government gives price floors and/or ceilings for products, rent, wages, etc. This article is an in-depth investigation of the effect of price controls like rent control and minimum wage on the efficiency of an economy. Importance of Price Controls Price controls are a very important part of any market. They play very important roles in protection of consumers Continue reading

Neoclassical Theory of Labor Supply Explained

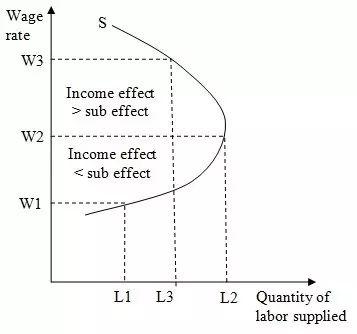

The total number of hours that an individual is capable and willfully supplies at a standard wage rate is called the labor supply. Thus supply of labor involves individuals seeking to be employed for a given an agreed amount of wage. But the neoclassical theory of individual labor supply terms income and leisure as the major source of individual utility. Income that is generated by the individual from work is spent for the leisure activities, depending on the individual’s own preference. However, the changes in the market wage rate impacts the individual in two ways; an increase or decrease in the income and a shift from one activity to the other. In the longer term, the extreme increases and decreases in the wage rate may decline to unacceptable levels forcing individuals to exit the labor market, a situation known as voluntary unemployment. Therefore, the neoclassical theory of individual labor supply Continue reading

Market Economy – Overview, Features, Characteristics, Advantages and Disadvantages

A market economy can be defined as an economy in which the allocation of resources is determined only by their supply and the demand for them. Market economy can also be defined as an economic system in which economic decisions and the pricing of goods and services are guided solely by the aggregate interactions of a country’s citizens and businesses and there is little government intervention or central planning. To conclude, the market economic system is basically a system whereby private individuals take up the responsibility of allocating resources to the public and relies chiefly on market forces to determine prices. Countries practicing the market economic system tend to assume that the forces of demand and supply are the main determinants of what is right for a nation’s well-being. They {the countries} rarely experience government interventions such as price fixing, license quotas and industry subsidizations. In reality, the market economy Continue reading