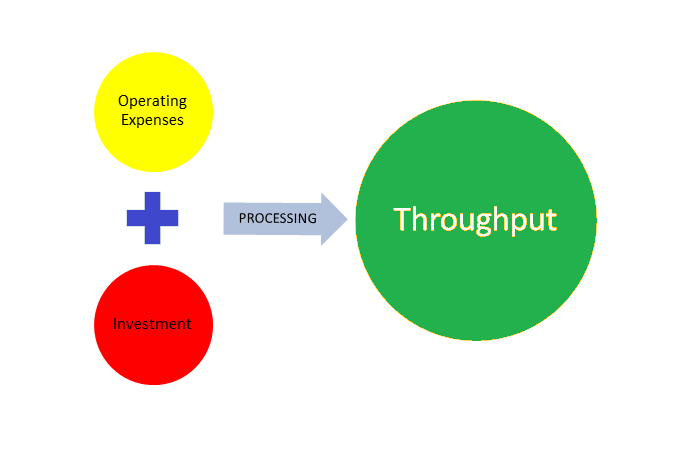

Goldratt’s ‘Throughput Accounting’ revolutionized the methods by which companies viewed their costs and associated them with profits. Unlike the traditional cost accounting methods, Goldratt argues that accounting should seek to maximize the movement of products through an organization to eliminate potential bottlenecks that prevents efficiency and speed. Goldratt argues that the current costing systems in use were developed almost a hundred years ago based upon the business practices and business designs of that particular era. The traditional accounting system therefore can be understood in the context of a “Cost World”. This cost world focuses all aspects of business value and decision making upon the cost of products themselves. In order to connect all of the subsequent aspects of business to costs, very elaborate allocation of expenses had to flow through to products. These “cost schemes” in effect have many different errors and assumptions that impacts the accuracy of accounts and Continue reading

Financial Accounting

Case Study on Business Ethics: Olympus Corporation Financial Statement Fraud

Olympus is a Japanese company that specializes in medical imaging tools and photo/video cameras. Back in the 1980s, when the operating income of the company decreased due to the sharp appreciation of the yen, the Olympus executives started an aggressive financial assets management in order to shift losses off the company’s balance sheet. As a result, Olympus has managed to hide $1.7 billion of investment losses for more than a decade. The case of Olympus is the example of the financial statement fraud in which an employee intentionally causes a misstatement or omission of material information in the organization’s financial reports that eventually results in median loss of $1 million. To conceal the losses, the company has developed a tobashi scheme in which they booked the company’s assets at historical cost instead of fair market value. In 1997, the Japanese legislation was reformed, and since then all the assets should Continue reading

Current Cost Accounting – Definition and Criticisms

Current Cost Accounting (CCA) attempts to provide more realistic book values by valuing assets at current market buying prices. It takes into account time-value of money and inflation. It is more complex than the traditional accounting, and it has created controversy about what adjustments are appropriate. Unlike Historical Cost Accounting, there is no need for inventory cost flow assumptions such as last-in-first-out and weighted average. The business profit in CCA shows how the entity has gained in financial terms the increase in cost of its resources, which is ignored by historical cost accounting. Differentiating operating profit from holding gains and losses has claimed to enhance the usefulness of information being provided by CCA. Holding gains are different from trading income as they are due to market-wide movements which are beyond the control of the management. Therefore, Current Cost Accounting doesn’t rewards managers for profits from holding gains and losses which Continue reading

Earnings Management – Meaning and Mechanism

The relationship between managers and shareholders in the business world cannot be disputable. This relationship is interpreted under Agency Theory. They are very dependent each other, even somehow there exist conflict of interest among these two parties. In example the shareholders put on trust to agency by contributing huge amount of money in terms of paid up capital, so that agency can generate business and obtain profit and increase the firm’s value as principles return. Meanwhile agency (managers) is dependent to the principles for remunerations and bonuses as compensation. Because of the great pressure from principles (shareholders) towards the high performance of firms values, so agency commonly practice earnings management in order to be sustained in market place. Earnings management may involve manipulation of accounting record, intentional omission or intentional misapplication of accounting o accounting principles. Earnings management is defined as the intentional misstatement of earnings leading to bottom line Continue reading

Importance of Financial Statements to External Users

In the presence of globalization, financial statements have become the standard measurement in judging a company’s performance. Financial statements are an overall impression of the company which shows profitability, efficient utilization of assets, settlement of outstanding debts, management of equity, and liquidity position to make economic and business decisions by both internal and external users. The analysis of financial statements is the application of financial activities and additional facts of the business, the examination of historical, present, and possible results and monetary situation to make investing, financing, and commercial decisions. External decision makers of an organization are defined as potential shareholders, clients, creditors (banks), and tax authorities who need a financial record to give decisions about investment, approval of loan application, acquisition of products, and compliance with applicable tax laws and regulations. This article will assess the importance of financial statements to external users in addition to a qualitative factor. Continue reading

Accounting Concepts Used for the Preparation of Financial Statements

Basic accounting concepts used for the preparation of financial statements are: Money measurement concept – Accounting normally deals with only those items that are capable of being expressed in monetary terms. Money has the advantage that it is a useful common denominator with which to express the wide variety of recourses held by a business. However, not all such resources are capable of being measured in monetary terms and so will be excluded from a balance sheet. The money measurement concept, thus, limits the scope of accounting reports. Historic cost concept – Assets are shown on the balance at a value that is based on their historic cost (that is, acquisition cost). This method of measuring asset value has been adopted by accountants in preference to methods based on some form of current value. Many commentators find this particular convection difficult to support as outdated historic cost are unlikely to Continue reading