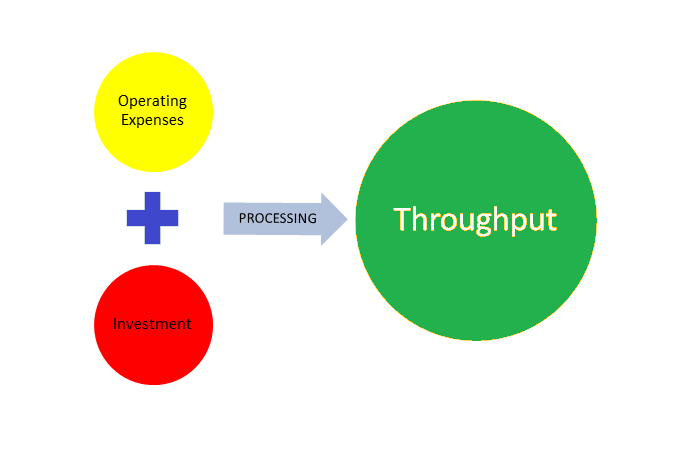

Goldratt’s ‘Throughput Accounting’ revolutionized the methods by which companies viewed their costs and associated them with profits. Unlike the traditional cost accounting methods, Goldratt argues that accounting should seek to maximize the movement of products through an organization to eliminate potential bottlenecks that prevents efficiency and speed. Goldratt argues that the current costing systems in use were developed almost a hundred years ago based upon the business practices and business designs of that particular era. The traditional accounting system therefore can be understood in the context of a “Cost World”. This cost world focuses all aspects of business value and decision making upon the cost of products themselves. In order to connect all of the subsequent aspects of business to costs, very elaborate allocation of expenses had to flow through to products. These “cost schemes” in effect have many different errors and assumptions that impacts the accuracy of accounts and Continue reading

Financial Accounting Concepts

Current Cost Accounting – Definition and Criticisms

Current Cost Accounting (CCA) attempts to provide more realistic book values by valuing assets at current market buying prices. It takes into account time-value of money and inflation. It is more complex than the traditional accounting, and it has created controversy about what adjustments are appropriate. Unlike Historical Cost Accounting, there is no need for inventory cost flow assumptions such as last-in-first-out and weighted average. The business profit in CCA shows how the entity has gained in financial terms the increase in cost of its resources, which is ignored by historical cost accounting. Differentiating operating profit from holding gains and losses has claimed to enhance the usefulness of information being provided by CCA. Holding gains are different from trading income as they are due to market-wide movements which are beyond the control of the management. Therefore, Current Cost Accounting doesn’t rewards managers for profits from holding gains and losses which Continue reading

What is Owner’s Equity? Meaning and Components

Preferred and common stockholders have some interests in organizations which are referred to as owner’s equity. Investors contribute to the capital of a corporation through the purchase of stocks sold by the corporation without the use of a secondary market. This type of capital is referred to as paid-in capital. The total paid-in capital is a combination of share capital and additional paid-in capital that is normally added to the nominal value of a stock. On the other hand, earned capital is the type of capital that comes from a company’s profitable operations. The two types of capital are normally reflected on the balance sheet as part of the owner’s equity. Earned capital is calculated by subtracting dividends from the total sum of the company’s beginning capital and the net income. The net income of a company is the major source of earned capital. Companies reinvest earned capital to generate more Continue reading

Earnings Management – Meaning and Mechanism

The relationship between managers and shareholders in the business world cannot be disputable. This relationship is interpreted under Agency Theory. They are very dependent each other, even somehow there exist conflict of interest among these two parties. In example the shareholders put on trust to agency by contributing huge amount of money in terms of paid up capital, so that agency can generate business and obtain profit and increase the firm’s value as principles return. Meanwhile agency (managers) is dependent to the principles for remunerations and bonuses as compensation. Because of the great pressure from principles (shareholders) towards the high performance of firms values, so agency commonly practice earnings management in order to be sustained in market place. Earnings management may involve manipulation of accounting record, intentional omission or intentional misapplication of accounting o accounting principles. Earnings management is defined as the intentional misstatement of earnings leading to bottom line Continue reading

Stakeholder, Institutional, and Legitimacy Theories of Accounting

A theory is defined as a set of principles that form the underlying structure that can be referred to in a discipline of study. Accounting, being a human activity, considers such things as the behavior of people and their needs in regard to information that is financial in nature. It also considers why an organisation might choose to divulge or give information to a particular group of stakeholders. The theories of accounting date back to the early 1920’s when researchers were basically relying on observation. All through this period, there has been an attempt to prescribe how assets should be valued for the sake of external reporting, predict on what basis managers should be paid or motivated, predict the power of different stakeholders, and how the organisation aspires to be judged by the community. This article will discuss three accounting theories namely the stakeholder theory, legitimacy theory and institutional theory. Continue reading

Approaches to Accounting Theories

Accounting theory is a set of basic assumptions, definitions, principles, and concepts surrounding the accounting rule. It includes the reporting of accounting and financial information to relevant or interested parties. There are several approaches that are used in the development of accounting theory. The two main ones are normative theory approach and the positive theory approach. Normative theory approach is a theory that is not based on observation. It is based on how things in the accounting process should be done. This approach comprises of different approaches to have a single but effective accounting approach. This kind of approach uses a formula to come up with an income based on value, not costs. On the other hand, positive or descriptive theoretical approach to accounting theory is a set of theories that is concerned with what accountants actually do. These theories rely on a process of inductive thinking, which involves making Continue reading