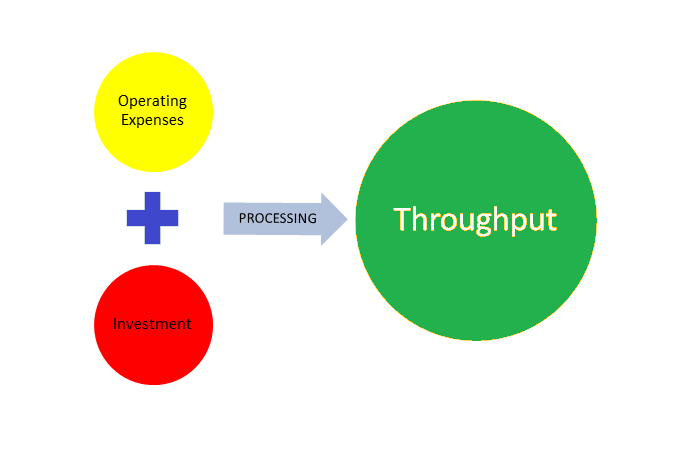

Goldratt’s ‘Throughput Accounting’ revolutionized the methods by which companies viewed their costs and associated them with profits. Unlike the traditional cost accounting methods, Goldratt argues that accounting should seek to maximize the movement of products through an organization to eliminate potential bottlenecks that prevents efficiency and speed. Goldratt argues that the current costing systems in use were developed almost a hundred years ago based upon the business practices and business designs of that particular era. The traditional accounting system therefore can be understood in the context of a “Cost World”. This cost world focuses all aspects of business value and decision making upon the cost of products themselves. In order to connect all of the subsequent aspects of business to costs, very elaborate allocation of expenses had to flow through to products. These “cost schemes” in effect have many different errors and assumptions that impacts the accuracy of accounts and Continue reading

Financial Concepts

Real Options in Capital Budgeting

Real options refer to a relatively new financial analytical tool that helps investors and managers to select market valuations that reflect a blend of businesses that are already known together with the value of business opportunities that are likely to arise. The Black-Scholes model is one of the best known forms of financial option theory that is applied through real options. There is need for managers and investors to understand how to take advantage of rapid changes that are occurring in economic world. This need if fulfilled by real options which gives them requisite insights into strategic investments and businesses. Real options are viable where particular conditions are met. Managers who are keen on maintaining the status quo will certainly miss the opportunities availed by this analytical tool. Economic changes occurring from time to time are a fertile breeding ground for real options. Businesses with adequate capital, reputable and intelligent Continue reading

Depreciation – Definition, Methods, and Tax Implications

Depreciation is a cost estimation method for accounting for the worth of a long-term asset over its useful life. Depreciation is used to spread the cost of a tangible asset over the accounting periods in which the asset is used. There are some questions surrounding this topic that are essential to explore. For instance, what are the tax implications of depreciation? What are the different depreciation methods, and how can they be used to calculate the amount? What are the best practices for managing depreciation? How does depreciation help to ensure a company’s financial health? Each of these questions will be explored in more detail to understand the concept of depreciation fully. Since antiquity, depreciation has been utilized for cost apportionment. Initially, the idea was developed by the Greek philosopher Aristotle, who believed that the value of an asset declined over time. By the 19th century, Italian economist Vilfredo Pareto Continue reading

Risks Associated with Derivatives

Although derivatives are legitimate and valuable tools for hedging risks, like all financial instruments they create risks that must be managed. Warren Buffett, one of the world’s most wise investors, states that “derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal.” On one hand derivatives neutralize risks while on the other hand they create risks. In fact there are certain risks inherent in derivatives. Derivatives can be dangerous if not managed properly. Numerous financial disasters such as Enron can be related to the mismanagement of derivatives. In the 1990s, Procter & Gamble lost $157 million in a currency speculation involving dollars and German Marks, Gibson Greetings lost $20 million and Long-Term Capital Management, a hedge fund, lost $4 billion with currency and interest-rate derivatives. It is key to consider that it has not been the use of derivatives as a tool which has Continue reading

Credit Rating – Meaning, Definition, Objectives, Approaches and Methodology

Credit rating is a codified rating assigned to an issue by authorized credit rating agencies. These agencies have been promoted by well-established financial Institutions and reputed banks/finance companies. Credit rating is a relative ranking arrived at by a systematic analysis of the strengths and weaknesses of a company and debt instrument issued by the company, based on financial statements, project analysis, creditworthiness factors and future prospectus of the project and the company appraised at a point of time. Objectives of Credit Rating Credit rating aims to: Provide superior information to the investors at a low cost; Provide a sound basis for proper risk-return structure; Subject borrowers to a healthy discipline, and Assist in the framing of public policy guidelines on institutional investment. Thus, credit rating in financial services represent an exercise in faith building for the development of a healthy financial system. Approaches to Credit Rating As a technique for Continue reading

Role of Financial Statements Analysis in Making Investment Decisions

One of the most important long-term decisions for any business is investment with the aim of making gains in the future. Investment decisions are concerned with the use of funds including buying, holding or selling and each decision could be vital to a firm. A careless decision may result in a long-term loss or even worse, bankruptcy. Therefore, an in-depth understanding and analysis is necessary for a high quality investment decision process. This is also even more critical to investors who invest in stock of company or shareholders. Financial statement analysis is critical in making effective stock investment decisions. By study the balance sheet, income statement, cash flow statement and statement of owners’ equity separately and combined, an analyst might have a good sense of a company’s overall financial picture; therefore, the investment decisions are likely to be reasonable and profitable. Financial Statements Analysis In order to understand the analysis Continue reading