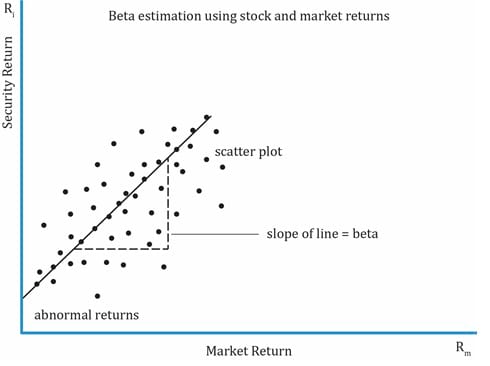

In finance, the Beta (β) of a stock or portfolio is a number describing the correlated volatility of an asset in relation to the volatility of the benchmark that said asset is being compared to. This benchmark is generally the overall financial market and is often estimated via the use of representative indices, such as the S&P 500, Nifty, Sensex, etc. Beta is also referred to as financial elasticity or correlated relative volatility, and can be referred to as a measure of the sensitivity of the asset’s returns to market returns, its non-diversifiable risk, its systematic risk, or market risk. On an individual asset level, measuring beta can give clues to volatility and liquidity in the marketplace. In fund management, measuring beta is thought to separate a manager’s skill from his or her willingness to take risk. The beta coefficient was born out of linear regression analysis. It is linked to a regression analysis of the returns of a portfolio (such as a stock index) (x-axis) in a specific period versus the returns Continue reading

Financial Management Concepts

Beyond Budgeting Approach

A traditional budget is usually prepared by reviewing past year’s budget and actual expenses, with addition or deduction towards extra business activities or reduced business activities planned and also by effecting changes towards changing factors, such as growth, inflation etc. It is basically to tie managers to predetermined actions in order to achieve the planned budget. It is usually based on organizational hierarchy and centralized leadership. In a business that operates in a very dynamic, rapidly changing, and innovative environment, traditional budgeting is inappropriate to exercise. Budget is a barrier for the business because the vibrant market demands flexibility, fast response, innovation, process improvement, customer focus, and shareholder value. And it is the limitation of the traditional budgeting not to be able to fulfill these demands. The dynamic driven business should keep up with the change and adaptive to recent development to achieve success. Hence Beyond Budgeting approach introduced. The Continue reading

Why Shareholder Wealth Maximization is Important in Business?

In modern finance, it is proven that shareholder wealth maximization is the superior goal of a firm and shareholders are the residual claimants; therefore maximizing shareholder returns usually implies that firms must also satisfy stakeholders such as customers, employees, suppliers, local communities, and the environment first. Also, a firm’s value can not be maximized if the management board or shareholders ignores the interest of its stakeholders. Thus, the main goal of a firm is to maximize shareholder wealth but it does not mean that management should disregard stakeholders. To begin with, it is necessary to understand what is shareholder wealth and why maximizing shareholder wealth is a superior objective? Maximizing shareholder wealth is defined as maximizing purchasing power as well as the flow of dividends to shareholders through time and it is a long-term perspective. In addition, a very important point to explain why shareholder wealth maximization is superior objective Continue reading

Forex Market or Foreign Exchange Market – History, Definition, Characteristics and Parties Involved

Foreign exchange refers to money denominated in the currency of another nation or group of nations. Foreign exchange can be cash, bank deposits or other short-term claims. But in the foreign exchange market as the network of major foreign exchange dealers engaged in high-volume trading, foreign exchange almost always take the form of an exchange of bank deposits of different national currency denominations. A Foreign exchange market or Forex market is a market in which currencies are bought and sold. It is to be distinguished from a financial market where currencies are borrowed and lent. Short History of the Foreign Exchange Market Foreign exchange markets mainly established to make easy cross border trade in which there is involvement of different currencies by governments, companies and individual investors. More ever these markets generally existed to supply for the international movement of capital and money, even the initial markets had speculators. Today, Continue reading

Cost Accounting – Definition, Objectives, Scope and Limitations

DEFINITION OF COST ACCOUNTING An accounting system is to make available necessary and accurate information for all those who are interested in the welfare of the organization. The requirements of majority of them are satisfied by means of financial accounting. However, the management requires far more detailed information than what the conventional financial accounting can offer. The focus of the management lies not in the past but on the future. For a businessman who manufactures goods or renders services, cost accounting is a useful tool. It was developed on account of limitations of financial accounting and is the extension of financial accounting. The advent of factory system gave an impetus to the development of cost accounting. Cost Accounting is a method of accounting for cost. The process of recording and accounting for all the elements of cost is called cost accounting. The Institute of Cost and Works Accountants, London defines Continue reading

Theories of Capital Structure

In practice it is difficult to specify an optional capital structure-indeed, managers even feels uncomfortable about specifying an optional capital structure range. Thus, financial managers worry primarily about whether their firms are using too little or too much debt, not about the precise optimal amount of debt. Even if a firm’s actual capital structure varies widely from the theoretical optimum, this capital structure decisions are secondary in importance to operating decisions, especially those relating to capital budgeting and the strategic direction of the firm. Different kinds of theories have been propounded by different authors to explain the relationship between capital structures. The four important theories of capital structure are: 1. Net Income Approach: According to this approach, a firm can minimize the weighted average cost of capital and increase the value of the firm as well as market price of equity shares by using debt financing to the maximum possible Continue reading