Working capital is said to be the life blood of a business. Working capital signifies funds required for day-to-day operation of the firm. In financial literature, there exist two concepts of working capital namely: gross and net. Accordingly, gross concept working capital refers to current assets viz: cash, marketable securities, inventories of raw materials, work-in-process, finished goods and receivables. According to net concept, working capital refers to the difference between current assets and current liabilities. Ordinarily, working capital can be classified into fixed or permanent and variable or fluctuating parts. The minimum level of investment in current assets regularly employed in business is called fixed or permanent working capital and the extra working capital needed to support the changing business activities is called variable or fluctuating working capital. There are broadly 3 working capital management strategies/ approaches to choose the mix of long and short-term funds for financing the net working Continue reading

Financial Management

Financial management entails planning for the future of a person or a business enterprise to ensure a positive cash flow, including the administration and maintenance of financial assets. The primary concern of financial management is the assessment rather than the techniques of financial quantification. Some experts refer to financial management as the science of money management. The five basic components of the Financial Management Framework are: Planning and Analysis, Asset and Liability Management, Reporting, Transaction Processing and Control.

Financial Analysis – Meaning, Definition and Methods

Financial statements are the source of information that present the economic value of a company to the external users. Several articles and books has defined the Financial analysis as to combine financial statement, financial notes, with other information, to evaluated the past, current, and future performance and financial position of company for the purpose of making investment, credit, and other economics decision. Financial Analysis is concerned with risk factors that might affect the future performance of a certain company. Financial analysis is concerned with different aspects of the company, in general financial analysis deals with profitability (ability to generate profit from delivering good and services), cash- flow generating ability (ability to generate cash inflows exceed cash outflows), liquidity (the ability to meet short term obligation), and solvency (the ability to meet long term obligation). In order to conduct a full, comprehensive analysis, analyst must collect information concerning economy, industry, competitors, Continue reading

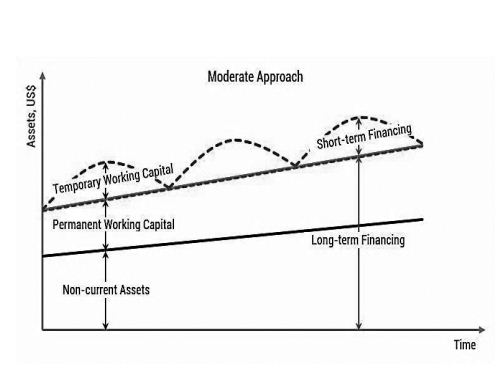

Principles of Working Capital Management

Working capital management is concerned with the problem that arises in attempting to manage the current assets, the current liabilities and the inter-relationship that exist between them. The goal of working capital management is to manage a firm’s current assets and current liabilities in such a way that a satisfactory level of working capital is maintained. The financial manager must keep in mind the following principles of working capital management: Principle of Optimization:The level of working capital must be so kept that the rate of return on investment is optimized. In other words, the working capital should be maintained at an optimum level. This is the point at which the increase in cost due to decline in working capital is equal to the increase in the gain associated with it. According to the principle of optimization, the magnitude of working capital should be such that each rupee invested adds to Continue reading

Total Return Swaps (TRS)

Total Return Swaps (TRS), sometimes known as a total rate of return swaps or TR swaps, are an on off-balance sheet transaction for the party who pays total returns composed of capital gains or losses plus the ordinary coupon or dividend, and receives LIBOR plus spread related to the counterparty’s credit riskiness on a given notional principal. The bank paying total returns is effectively warehousing, renting out its balance sheet while transferring economic value and risk to preferably an uncorrelated counterparty to the referenced assets. A TRS is similar to a plain vanilla swap except the deal is structured such that the total return (cash flows plus capital appreciation/depreciation) is exchanged, rather than just the cash flows. It is one of the principal instruments used by banks and other financial instruments to manage their credit risk exposure, and as such is a credit derivative. They are used as credit risk Continue reading

The Importance of Credit Risk Management in Banking

Credit risk implies a potential risk that the counterparty of a loan agreement is likely to fail to meet its obligations as per the original loan agreement, and may eventually default on the obligation. Credit risks can be classified into many forms such as options, equities, mutual funds, bonds, loans, and other financial issues as well, which in extensions of guarantees and the settlement of these transactions. Is it Important for the Banks to Manage their Credit Risks? Risk is always associated with banking activities, and taking a risk is an important part of any banking operation, there is hardly any banking operation without the risk. Most of the bankers are said to be sound when they have a clear overview of what is the amount of risk involved in the current transaction and they make sure that some of the partly earnings are therefore kept for these risks. The Continue reading

The Advantages and Disadvantages of Budgeting

A budget can be described as a financial plan for a business that has been prepared well in advance to demonstrate and dictate the future course of work of a business. A budget may be set in money terms or it can be expressed in terms of units. Budgets can also be put across in the form of income budgets for money received i.e. sales budget, or expenditure budgets for money spent, i.e. a purchases budget. However, a major emphasis has always been on the cash budget which combines both income and expenditure in estimating the business working capital, cash in hand and bank balance during a course of work or a time period. The budgets are usually prepared for the following financial years (budget period), and are usually broken down into shorter time periods in order to emphasize on the figures and their attainment/fulfillment. The periods are usually monthly Continue reading