Financial accounting and management accounting play an important part in accounting information system. They co-exist in enterprise production and operation of management, constituting the modern enterprise accounting system together. Much information which management accounting required is from financial accounting, while financial accounting also put the established budget, standards organizations, and such daily accounting data from management accounting as the basic premise. Management accounting is used primarily by those within a company or organization. Reports can be generated for any period of time such as daily, weekly or monthly. Reports are considered to be “future looking” and have forecasting value to those within the company. Main function of management accounting in the enterprise is to establish a variety of internal accounting control system and provide internal management needs of a variety of data and information at the aim of improving operational efficiency and effectiveness. Financial accounting is used primarily by those Continue reading

Financial Management

Financial management entails planning for the future of a person or a business enterprise to ensure a positive cash flow, including the administration and maintenance of financial assets. The primary concern of financial management is the assessment rather than the techniques of financial quantification. Some experts refer to financial management as the science of money management. The five basic components of the Financial Management Framework are: Planning and Analysis, Asset and Liability Management, Reporting, Transaction Processing and Control.

Problems in Determination of Cost of Capital

It has already been stated that the cost of capital is one of the most crucial factors in most financial management decisions. However, the determination of the cost of capital of a firm is not an easy task. The finance manager is confronted with a large number of problems, both conceptual and practical, while determining the cost of capital of a firm. These problems in determination of cost of capital can briefly be summarized as follows: 1. Controversy regarding the dependence of cost of capital upon the method and level of financing There is a, major controversy whether or not the cost of capital dependent upon the method and level of financing by the company. According to the traditional theorists, the cost of capital of a firm depends upon the method and level of financing. In other words, according to them, a firm can change its overall cost of capital Continue reading

Approaches to Accounting Theories

Accounting theory is a set of basic assumptions, definitions, principles, and concepts surrounding the accounting rule. It includes the reporting of accounting and financial information to relevant or interested parties. There are several approaches that are used in the development of accounting theory. The two main ones are normative theory approach and the positive theory approach. Normative theory approach is a theory that is not based on observation. It is based on how things in the accounting process should be done. This approach comprises of different approaches to have a single but effective accounting approach. This kind of approach uses a formula to come up with an income based on value, not costs. On the other hand, positive or descriptive theoretical approach to accounting theory is a set of theories that is concerned with what accountants actually do. These theories rely on a process of inductive thinking, which involves making Continue reading

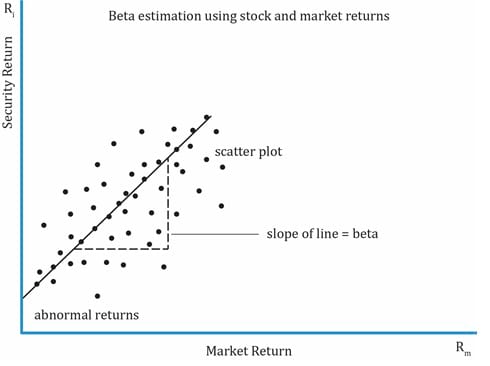

Stock Beta – Meaning, Calculation, Applications and Types

In finance, the Beta (β) of a stock or portfolio is a number describing the correlated volatility of an asset in relation to the volatility of the benchmark that said asset is being compared to. This benchmark is generally the overall financial market and is often estimated via the use of representative indices, such as the S&P 500, Nifty, Sensex, etc. Beta is also referred to as financial elasticity or correlated relative volatility, and can be referred to as a measure of the sensitivity of the asset’s returns to market returns, its non-diversifiable risk, its systematic risk, or market risk. On an individual asset level, measuring beta can give clues to volatility and liquidity in the marketplace. In fund management, measuring beta is thought to separate a manager’s skill from his or her willingness to take risk. The beta coefficient was born out of linear regression analysis. It is linked to a regression analysis of the returns of a portfolio (such as a stock index) (x-axis) in a specific period versus the returns Continue reading

Beyond Budgeting Approach

A traditional budget is usually prepared by reviewing past year’s budget and actual expenses, with addition or deduction towards extra business activities or reduced business activities planned and also by effecting changes towards changing factors, such as growth, inflation etc. It is basically to tie managers to predetermined actions in order to achieve the planned budget. It is usually based on organizational hierarchy and centralized leadership. In a business that operates in a very dynamic, rapidly changing, and innovative environment, traditional budgeting is inappropriate to exercise. Budget is a barrier for the business because the vibrant market demands flexibility, fast response, innovation, process improvement, customer focus, and shareholder value. And it is the limitation of the traditional budgeting not to be able to fulfill these demands. The dynamic driven business should keep up with the change and adaptive to recent development to achieve success. Hence Beyond Budgeting approach introduced. The Continue reading

Why Shareholder Wealth Maximization is Important in Business?

In modern finance, it is proven that shareholder wealth maximization is the superior goal of a firm and shareholders are the residual claimants; therefore maximizing shareholder returns usually implies that firms must also satisfy stakeholders such as customers, employees, suppliers, local communities, and the environment first. Also, a firm’s value can not be maximized if the management board or shareholders ignores the interest of its stakeholders. Thus, the main goal of a firm is to maximize shareholder wealth but it does not mean that management should disregard stakeholders. To begin with, it is necessary to understand what is shareholder wealth and why maximizing shareholder wealth is a superior objective? Maximizing shareholder wealth is defined as maximizing purchasing power as well as the flow of dividends to shareholders through time and it is a long-term perspective. In addition, a very important point to explain why shareholder wealth maximization is superior objective Continue reading