A lot has been said about open economies but the fact is that their existence is only in theory. It is common knowledge that all countries in the world have some entry restrictions in their markets. With this in mind, open economies are described as those countries whose policies allow production and pricing to be determined by the forces of supply and demand. The aforementioned restrictions are, therefore, in the form of policies that countries develop in a bid to accelerate economic growth. One of such policies is price control in which a government gives price floors and/or ceilings for products, rent, wages, etc. This article is an in-depth investigation of the effect of price controls like rent control and minimum wage on the efficiency of an economy. Importance of Price Controls Price controls are a very important part of any market. They play very important roles in protection of consumers Continue reading

Managerial Economics

Managerial Economics generally refers to the integration of economic theory with business practice. It deals with the use of economic concepts and principles of business decision making. Managerial Economics is thus constituted of that part of economic knowledge or economic theories which is used as a tool of analyzing business problems for rational business decisions. Managerial economics can be viewed by most modern economists as a practical application of economics theory in using effectively the firms scarce resources.

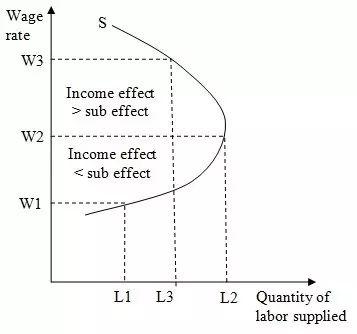

Neoclassical Theory of Labor Supply Explained

The total number of hours that an individual is capable and willfully supplies at a standard wage rate is called the labor supply. Thus supply of labor involves individuals seeking to be employed for a given an agreed amount of wage. But the neoclassical theory of individual labor supply terms income and leisure as the major source of individual utility. Income that is generated by the individual from work is spent for the leisure activities, depending on the individual’s own preference. However, the changes in the market wage rate impacts the individual in two ways; an increase or decrease in the income and a shift from one activity to the other. In the longer term, the extreme increases and decreases in the wage rate may decline to unacceptable levels forcing individuals to exit the labor market, a situation known as voluntary unemployment. Therefore, the neoclassical theory of individual labor supply Continue reading

Market Economy – Overview, Features, Characteristics, Advantages and Disadvantages

A market economy can be defined as an economy in which the allocation of resources is determined only by their supply and the demand for them. Market economy can also be defined as an economic system in which economic decisions and the pricing of goods and services are guided solely by the aggregate interactions of a country’s citizens and businesses and there is little government intervention or central planning. To conclude, the market economic system is basically a system whereby private individuals take up the responsibility of allocating resources to the public and relies chiefly on market forces to determine prices. Countries practicing the market economic system tend to assume that the forces of demand and supply are the main determinants of what is right for a nation’s well-being. They {the countries} rarely experience government interventions such as price fixing, license quotas and industry subsidizations. In reality, the market economy Continue reading

Monopsony and Competition Law in Indian Context

Can a buyer be the biggest bully? The classical theory of monopsony answers this question. It envisions a market scenario with only one buyer, who can use his leverage to reduce the quantity of product purchased, thereby driving down the price that he has to pay. Seldom does a monopsonistic situation arise in the market, so much so that little has been thought till date about the potential adverse impact of such a scenario on market competition. Another reason for the antitrust analyst’s apparent neglect of the power on the buyer’s side of the market may be that such power tends to reduce the selling price of a commodity, thereby causing a prima facie increase in consumer welfare, which has always been one of the traditional goals of competition law. Classical Monopsony -What does It Entail? Pure monopsony can be looked upon as the demand-side analogue of the monopolist who Continue reading

Comparison of Different Economic Systems

Any system that involves the mechanism for production, distribution and exchange of goods apart from consumption of the goods and services within the different entities can be classified as an Economic System. The various kinds of economic systems and their classifications broadly follow the methods by which means of ownership are established. Thus, the mode of ownership of capital leads to the different kinds of economic systems in vogue. This article focuses on three types of economic systems, such as market, command, and mixed economy. It compares and contrasts these types in terms of the role of the government in their functioning, property and land ownership, mechanisms of price formation, division of labor, and income distribution. Market Economy vs. Command Economy A market economy can be described as an economic system where the production means are largely privately owned and aimed at profit and the process of capital accumulation. In Continue reading

Alfred Chandler’s Model of Integrated Managerial Enterprise

Managerial enterprises received the priority and governmental focus in the modern economic strategy that led to the fast and impressive growth of the economies of developed countries. Numerous countries have chosen the model designed by Alfred Chandler as the primary tool for changing the perspectives and visions to transform and grow to become powerful national economic enterprises. The model is based on the economic logic. The decisions made by managers based on this approach had a momentous impact on the path of economic advancement of Germany making this country one of the most influential players in the global arena, increasing production level in the United States, and helped Japan reach its leading position in the world. Adherence to the economic logic became the engine for the economic improvement. However, weak implementation of the Chandler’s model consequently led the United States to the decline in the competitiveness in machinery and electronics Continue reading