In case of Marginal Cost Pricing we have to consider the incremental cost of production. Fixed cost is not taken into consideration. Marginal cost is the additional cost for producing additional unit of output. In this method the price is related to marginal cost. The main difference between Full Cost Pricing and Marginal Cost Pricing is that in Marginal Cost Pricing the fixed cost component is not included. The Marginal Cost Pricing is useful in the short period whereas Full Cost Pricing is mainly for the long period. As long as the marginal cost is covered there is a sort of guarantee that the firm will not shut down. Advantages of Marginal Cost Pricing Variable cost remains constant per unit of output and fixed costs remain constant in total during short period. Thus control over costs becomes more effective and easier. Standards can be set for variable costs, while Budgets Continue reading

Economics Principles

Demand Curve under Different Market Structures

Firm Demand (company demand) denotes the demand for the product/s of a particular firm. While Industry demand means the demand for the product of a particular industry. An industry comprises all the firms or companies producing similar products which are quite close substitutes to each other irrespective of the differences in their brand names. To understand the relation between company and industry demand necessitates an understanding of different market structures. The demand curve of an individual firm is not the same as the industry or market demand curve except in case of monopoly. Monopoly is that market category in which there is only a single seller and therefore there is no difference between a firm and an industry. The firm is itself an industry and therefore the demand curve of the individual firm as well as the industry demand curve under monopoly will be the same and as we shall Continue reading

Three Concepts of Poverty – Economic wellbeing, Capability, and Social Exclusion

Poverty – A Multidimensional Phenomenon Poverty has many faces, and multiple indicators are used to capture the different deprivations experienced by a population. This complex phenomenon is linked to economic wellbeing, capability, and social exclusion. Poverty is a major moral problem because of the suffering it causes and the disadvantages conferred to some population segments. It is defined as a persistent and debilitating social condition attributed to diverse causes that affect a person’s physical, mental, and emotional wellbeing. The complex nature of poverty means that multiple measures are used depending on a country’s priorities. 1. Economic Wellbeing Income and consumption are key quantifiable indicators of poverty in society. These variables measure economic wellbeing and contain absolute, relative, and subjective components. At the basic level is absolute poverty, which describes the lack of necessities needed for survival – shelter, clean water, and food. Here, the quality of survival is an important Continue reading

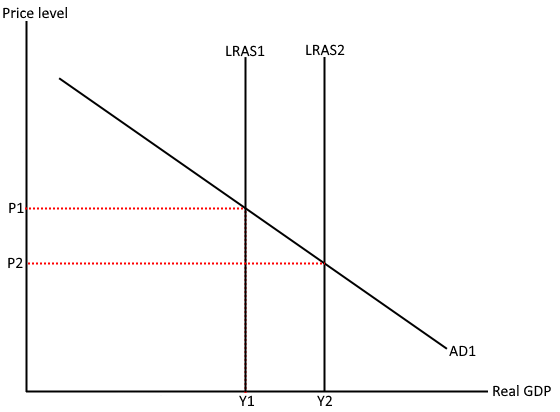

Supply Side Policies – Meaning, Definition, and Categories

The supply side policies entail the attempts undertaken by governments in an effort to stimulate productivity and ensure that the long-term aggregate supply [LRAS] curve shifts to the right as illustrated in graph 1 below. The outward shift of the LRAS curve leads to an increase in the potential output. From the graph, the shift in the LRAS to LRAS2 leads to an increase in the size of the output from Y1 to Y2. The supply side policies are focused on stimulating a country’s productive capacity. Labor productivity is one of the most important elements in the supply side policies. The policies underscore the importance of establishing flexible labor markets. Despite the flexibility aspect, the role of the government in the implementation of the supply side policies cannot be ruled out. In some instances, government intervention is necessary in order to overcome market failure. The objective of the supply side Continue reading

Profit Maximization Model in Managerial Economics

Profit-making is one of the most traditional, basic and major objectives of a firm. Profit-making is the driving-force behind all business activities of a company. It is the primary measure of success or failure of a firm in the market. Profit earning capacity indicates the position, performance and status of a firm in the market. It is an acid test of economic ability and performance of an individual firm. There is no place for a firm unless it earns a reasonable amount of profit in the business. It is necessary to stay in business and maintain in tact the wealth producing agents. It is a widely accepted goal and there is nothing bad or immoral about it. Earlier profit maximization was the sole objective of a firm. This assumption has a long history in economic literature and the conventional price theory was based on this very assumption about profit making. Continue reading

Different Approaches to Profit in Managerial Economics

Profit is the reward which goes to organization as a factor of production for its participation in the process of production. Profits differ from other factor rewards in the following ways: Profit is a residual income left after the payment of contractual rewards to other factors of production. The entrepreneur while hiring other factors of production enters into contract with them. He pays wages to workers, rent for land and interest for borrowed capital and the residue or whatever is left is his profit. Thus profits become non-contractual in character. The various factors of production are rewarded even before the sale of the product and irrespective of its sales whereas profits accrue only after the product is sold. The rewards of other factors have been fixed. They do not fluctuate whereas profits go on fluctuating so much so that the entrepreneur bears the risk of even incurring losses which we Continue reading